by Team NeuroTrade

56

The Volume-Weighted Average Price (VWAP) is a very famous and actually very useful indicator for intraday traders. Which tells you the price of a particular security, weighted by volume. Most of the intraday traders use VWAP for trade direction confirmation in their trading system.

If you want to calculate with Python code, then below is the required code.

1. Setting Up your working Environment

Install the required libraries:

pip install pandas yfinanceIn our code we required a pandas dataframe to process the data with column names Open, High, Low, Close, and Volume.

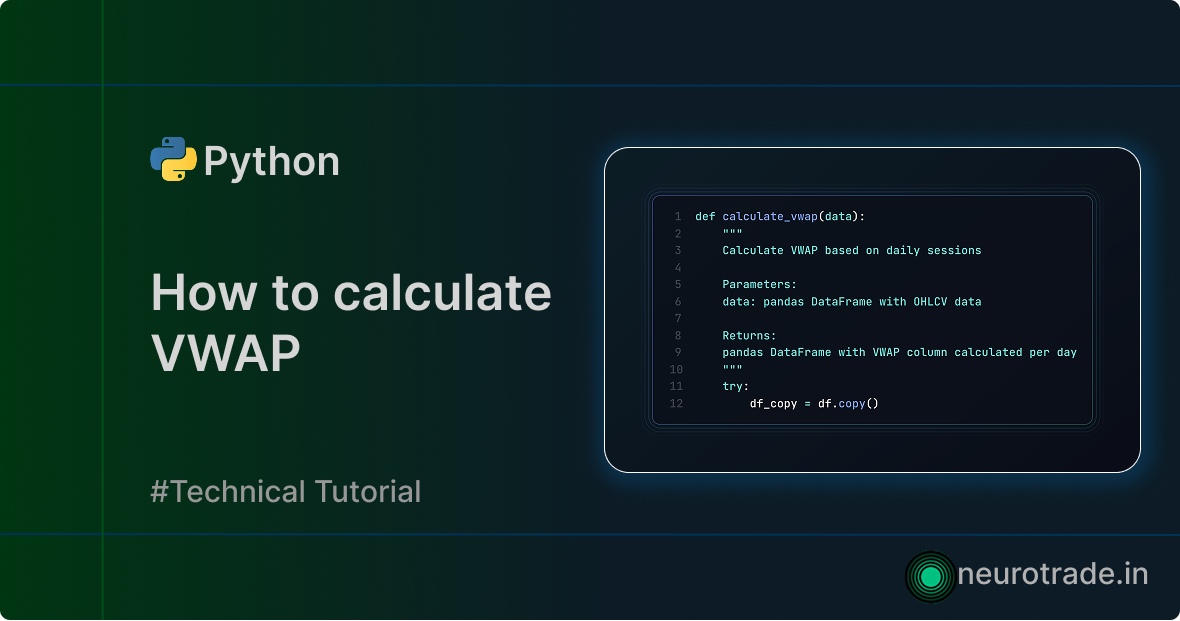

2. Code for VWAP

def calculate_vwap(df, time_column='time'):

"""

Calculate VWAP based on daily sessions

Parameters:

df: pandas DataFrame with OHLCV data

time_column: str, name of the time/datetime column (default: 'time')

Returns:

pandas DataFrame with VWAP column calculated per day

"""

try:

df_copy = df.copy()

# Ensure time column is datetime

if not pd.api.types.is_datetime64_any_dtype(df_copy[time_column]):

df_copy[time_column] = pd.to_datetime(df_copy[time_column])

# Extract date for grouping (removes time component)

df_copy['date'] = df_copy[time_column].dt.date

# Function to calculate VWAP for each group (day)

def calc_daily_vwap(group):

# Calculate typical price

group['typical_price'] = (group['High'] + group['Low'] + group['Close']) / 3

# Calculate price * volume

group['price_volume'] = group['typical_price'] * group['Volume']

# Calculate cumulative values within the day

group['cum_price_volume'] = group['price_volume'].cumsum()

group['cum_volume'] = group['Volume'].cumsum()

# Calculate VWAP

group['VWAP'] = group['cum_price_volume'] / group['cum_volume']

return group

# Apply VWAP calculation to each day

df_copy = df_copy.groupby('date', group_keys=False).apply(calc_daily_vwap)

# Drop intermediate calculation columns

drop_columns = ["typical_price", "price_volume", "cum_price_volume", "cum_volume", "date"]

data = df_copy.drop(columns=drop_columns)

# Reset index to ensure clean DataFrame

data = data.reset_index(drop=True)

return data

except Exception as e:

exc_type, exc_obj, exc_tb = sys.exc_info()

print("Error is " + str(e) + " at " + str(exc_tb.tb_lineno))

return None

NOTE: You guys have to pass a pandas dataframe as the df input parameter.

Subscribe to our email list here to get the latest updates first in your inbox.